AFRICA INFRASTRUCTURE THESIS - Two Undervalued Digital & Telecom Infrastructure Companies Driving Economic Transformation

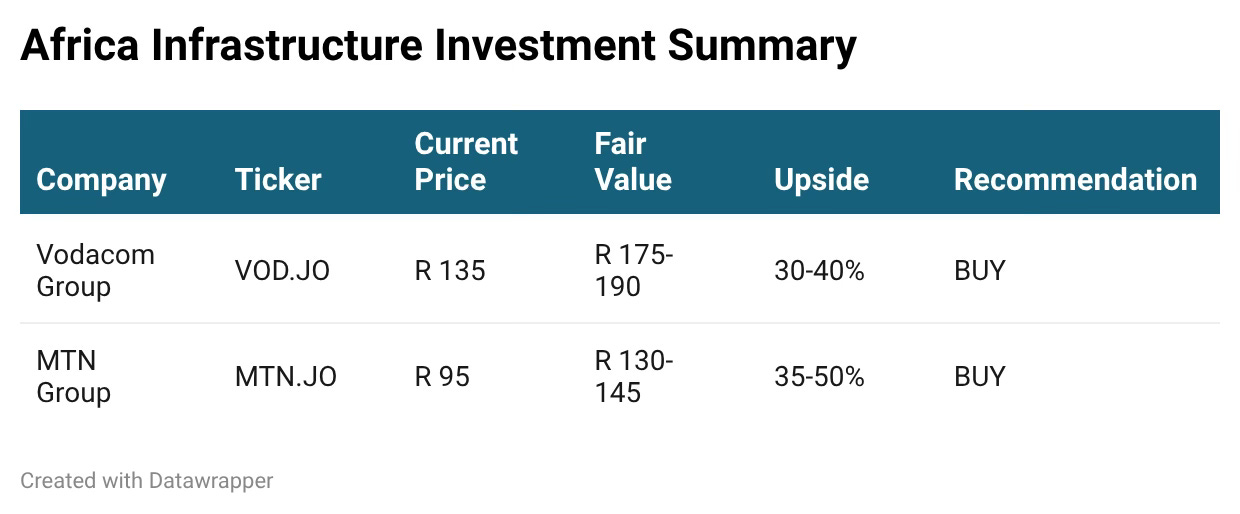

Vodacom Group (VOD.JO) | MTN Group (MTN.JO) Rating: BUY | Upside: 30-50%

SPHAERA Global Research

Published: February 18, 2026

Sector: Telecom Infrastructure / Emerging Markets

Geographic Focus: Sub-Saharan Africa

EXECUTIVE SUMMARY

Africa’s digital infrastructure build-out represents one of the most compelling investment opportunities in emerging markets. As Middle Eastern capital flows into renewable energy infrastructure and China deepens trade ties through tariff elimination, the continent’s telecom operators are positioned as critical enablers of economic transformation.

This report identifies Vodacom Group (VOD.JO) and MTN Group (MTN.JO) as BUY opportunities, trading at 30-50% discounts to intrinsic value while delivering double-digit revenue growth and expanding into high-margin fintech services.

Key Investment Thesis

✅ Africa’s mobile penetration: 50% (vs 80%+ in Asia) – massive runway for growth

✅ Fintech revolution: Mobile money processing $450B+ annually (Vodacom) and $212B (MTN)

✅ Infrastructure as geopolitical priority: China removing tariffs, Middle East investing $2.6B in power

✅ Telecom operators = digital rails enabling all transformation

✅ Both trading 30-50% below fair value despite strong fundamentals

THE AFRICA INFRASTRUCTURE CONVERGENCE

Three Forces Accelerating African Development

1. MIDDLE EASTERN CAPITAL DEPLOYMENT

Our recent research identified $2.6 billion in Middle Eastern renewable energy investment flowing into Ghana, Côte d’Ivoire, and Zambia. Masdar and ACWA Power are building grid infrastructure that requires telecom connectivity for:

Smart metering

Grid management systems

Mobile payment integration

Real-time monitoring

Every solar farm needs telecom. Every smart grid needs connectivity. Telecom operators are infrastructure enablers.

2. CHINA’S TRADE DEEPENING

China eliminated tariffs on 53 African countries effective May 1, 2026, opening 1.4 billion Chinese consumers to African exports. This accelerates:

E-commerce growth (requires mobile payments)

Cross-border digital services

Supply chain digitization

Trade finance platforms

All riding on telecom infrastructure.

3. DEMOGRAPHIC DIVIDEND

Africa population: 1.4 billion (2025) → 2.5 billion (2050)

Median age: 19 years (digital natives)

Smartphone adoption: Accelerating (65% penetration on Vodacom network)

Data usage: 12.4 GB/month per user (+17% YoY)

These aren’t feature phone users. They’re demanding smartphones, mobile money, streaming services, and fintech. The infrastructure must be built.

Why Telecom Infrastructure Matters

Power grids need telecoms for smart meters.

E-commerce needs mobile money.

Manufacturing needs IoT connectivity.

Agriculture needs mobile banking for smallholder farmers.

Education needs mobile internet.

Healthcare needs telemedicine.

Telecom operators aren’t just selling data plans – they’re building the digital rails that enable economic transformation.

VODACOM GROUP LIMITED (VOD.JO)

Company Snapshot

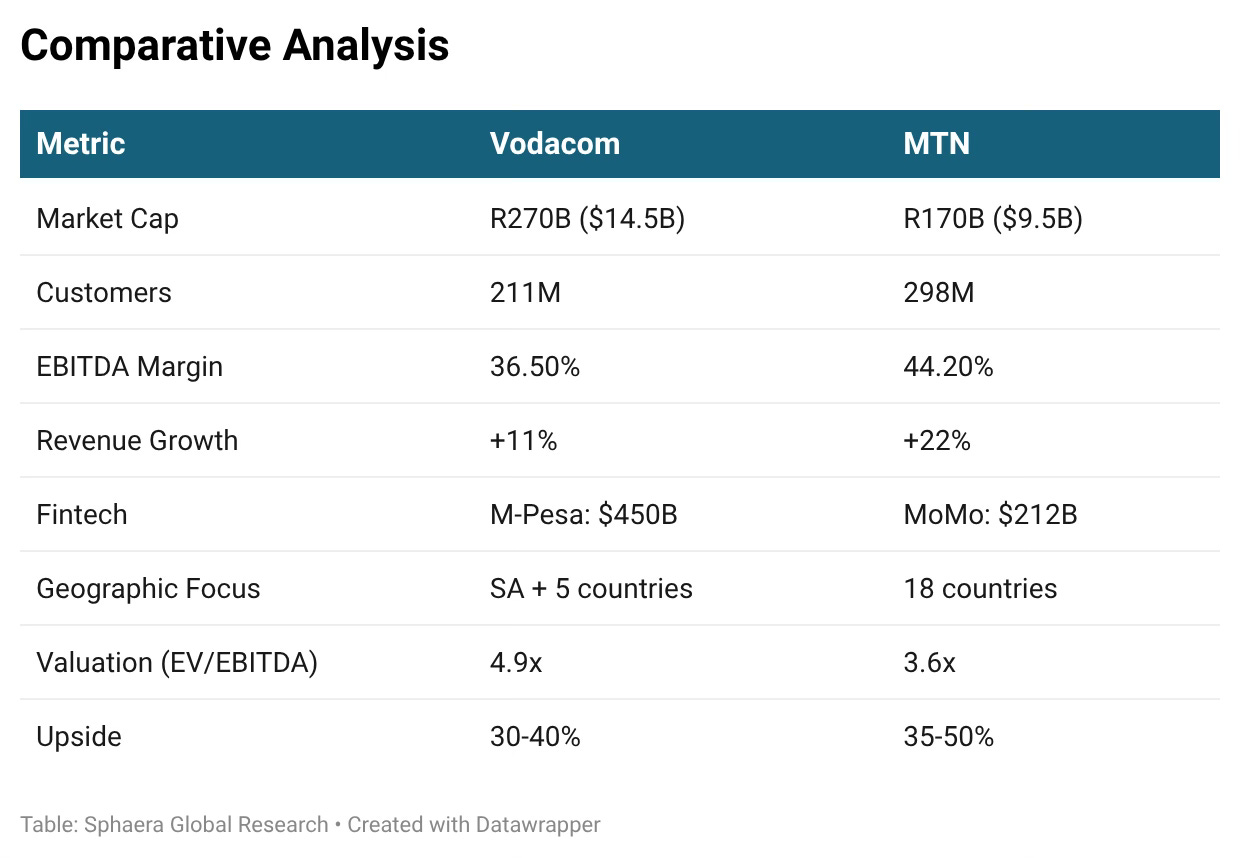

Market Cap: R270B (~$14.5B)

Customers: 211.3M (South Africa + International)

Revenue (FY2025): R152.2B (+10.9% normalized, +1.1% reported)

EBITDA: R55.5B (36.5% margin)

Current Price: R 135

The Hidden Value Story

The market sees: A South African telco with +1% reported revenue growth.

The reality: Currency fluctuations are masking +11% normalized growth and explosive fintech expansion.

M-Pesa: The $14B Fintech Platform

Revenue: R14B (~10% of total, growing 15-20%)

Transactions: $450B+ annually

Markets: Tanzania ($1.2B/month), Mozambique, DRC, Lesotho

Margins: 40-45% (vs 35% telecom)

M-Pesa isn’t just mobile money—it’s becoming the banking infrastructure for 211 million people.

Safaricom: The Undervalued Asset

Vodacom owns 34.94% of Safaricom (Kenya’s dominant telco) as of early 2026:

45M customers in Kenya

Market leader with ~65% share

Strong M-Pesa franchise

Government trying to acquire stake (signals value)

Market isn’t pricing this stake properly. Safaricom alone could be worth R20-30 per Vodacom share.

International Growth Engine

Tanzania:

26M customers (+19.8% revenue growth)

M-Pesa processing TZS 3T/month ($1.2B)

Network expansion ongoing

DRC:

17M customers

Low penetration = huge runway

Infrastructure sharing with Airtel (reduces capex 30-40%)

Mozambique: 6M customers, growing

Strategic Advantages

1. Infrastructure Sharing (Game Changer):

Airtel partnership (Aug 2025): Share towers in Mozambique, Tanzania, DRC

Reduces capex intensity from 15-20% to 10-13%

Expands margins from 35-40% to 40-45%

Not priced into analyst models

2. Starlink Partnership (Nov 2025):

Resell satellite services in 10+ markets

Enables entry into Zambia, Angola, Ethiopia without building towers

Enterprise revenue opportunity

Valuation

DCF Analysis:

WACC: 13.5%

Terminal growth: 3.5%

Fair value: R175-190

Comparable Analysis:

Vodacom trading at 4.9x EV/EBITDA

Peers (Airtel Africa, MTN) trading at 5.5-6.0x

Discount: 10-20% vs peers despite better margins

Base Case: R175 (30% upside)

Bull Case: R200-220 (48-63% upside with expansion execution)

Catalysts

Near-term (Next 6 months):

Q1 FY2026 Results (May 2026) – Confirm M-Pesa momentum

FY2026 Guidance – Expect management to raise medium-term targets

Medium-term (6-18 months):

Safaricom re-rating as Kenya economy improves

M-Pesa standalone valuation event (potential spin-off/separate listing)

Currency stabilization reveals true earnings power

Ongoing:

Dividend yield: 4-5% (90%+ payout ratio) – get paid while you wait

MTN GROUP LIMITED (MTN.JO)

Company Snapshot:

Market Cap: R170B (~$9.5B)

Customers: 297.7M across 18 African markets

Revenue (H1 2025): R105.1B (+22.4% constant currency)

EBITDA: R46.7B (44.2% margin, +7.1pp YoY)

Current Price: R 95

The Turnaround Story

MTN was written off 18 months ago due to Nigeria chaos, regulatory fines, and currency devaluations.

The market missed the inflection point.

Nigeria: From Disaster to Driver

Nigeria was MTN’s biggest problem (35% of revenue). Now it’s the growth engine:

Revenue: +54% growth (H1 2025)

Why: Naira stabilization (~1,600/USD vs 1,900 peak)

Catalyst: Tinubu government reforms working

Tailwind: Inflation moderating, FX market functioning

MoMo: The Fintech Explosion

Transaction value: $212.2B (+45.4% YoY)

Active users: 63M monthly

Advanced services: 33.4% of revenue (up from 29.6%)

Digital credit, savings, insurance, merchant payments

Growing +42% YoY

MoMo is becoming Africa’s banking infrastructure. 70% of Sub-Saharan Africa is unbanked. MTN is filling the gap.

The Margin Story

EBITDA margin: 44.2% (+7.1pp YoY)

This is operating leverage at scale. As data usage grows and fintech scales, margins expand:

More data on existing towers = incremental revenue, minimal cost

MoMo transactions = 50%+ margins

Infrastructure sharing = capex savings

IHS Towers Acquisition (MAJOR CATALYST)

Announced: February 17, 2026

Target: IHS Towers (Africa’s largest tower company)

Price: $8.50/share

Why this matters:

MTN becomes infrastructure landlord

Airtel, Vodacom, others pay rent to MTN

Vertical integration = cost savings + revenue opportunity

Strategic shift: From tower lessee to tower owner

This is Netflix moving from licensing content to producing it. Economics flip entirely.

Geographic Diversification = Resilience

MTN operates in 18 countries:

Nigeria: 35% (stabilizing)

South Africa: 20%

Ghana: 8% (+40% growth)

Rest of Africa: 37% (high growth)

One country blows up? 17 others keep running.

Balance Sheet Strength

Net debt/EBITDA: 0.5x (down from 0.7x)

OpFCF: R20.5B (doubled YoY)

Capacity: Firepower for IHS acquisition, future M&A, shareholder returns

Valuation

DCF Analysis:

WACC: 14%

Terminal growth: 4%

Fair value: R130-145

Comparable Analysis:

MTN trading at 3.6x EV/EBITDA

Peers trading at 6.0x EV/EBITDA

Discount: 40% vs peers

This is insane. MTN has better margin trajectory and fintech growth than peers, yet trades at 40% discount.

Base Case: R130-145 (35-50% upside)

Bull Case: R155-175 (63-84% upside with IHS + expansion)

Investment Thesis

✅ Nigeria turnaround: +54% growth, macro stabilizing

✅ MoMo explosion: $212B transactions (+45%), advanced services scaling

✅ Margin expansion: 44.2% (+7pp from operating leverage)

✅ IHS catalyst: Infrastructure landlord economics

✅ Upgraded guidance: Management raising targets (confidence signal)

✅ Valuation absurdity: 40% discount to peers despite better fundamentals

Rating: STRONG BUY | Target: R130-145 | Upside: 35-50%

VODACOM VS MTN: WHICH TO BUY?

Our Recommendation: BUY BOTH

These are not mutually exclusive opportunities.

Vodacom offers:

Exposure to stable South Africa

Safaricom growth story (Kenya)

M-Pesa fintech platform

Lower volatility

Defensive characteristics

MTN offers:

Pure-play pan-African growth

Nigeria turnaround (high risk, high reward)

Infrastructure control (IHS Towers)

Higher growth rates

Deeper value (bigger discount)

Suggested portfolio allocation:

60% Vodacom / 40% MTN for balanced risk/reward

Or 100% Vodacom if you want lower risk

Or 100% MTN if you want maximum upside

Both are undervalued. Both have catalysts. Both win as Africa digitizes.

THE MACRO BACKDROP: WHY NOW?

1. Capital Flows Accelerating Into Africa

Middle Eastern Renewable Investment:

$2.6 billion flowing into Ghana, Zambia, Côte d’Ivoire for solar and grid infrastructure. Every smart grid needs telecom connectivity.

Chinese Trade Deepening:

Zero tariffs for 53 African countries = e-commerce boom = mobile payment growth = telecom demand.

DFI Support:

World Bank, IFC, US DFC all increasing Africa allocations. Infrastructure is priority.

Private Equity Interest:

KKR, Carlyle, TPG raising Africa-focused funds. Capital is coming.

2. Smartphone Penetration at Tipping Point

Africa smartphone penetration: 65% (Vodacom network), up from 50% two years ago.

Tipping point dynamics:

First 50% adoption = slow (infrastructure build-out)

50-80% adoption = acceleration phase (network effects kick in)

80%+ adoption = mature/saturated

We’re entering the acceleration phase.

Average data usage: 12.4 GB/month (+17% YoY)

What this means: More data consumed = more revenue = more fintech transactions = compounding growth

3. Regulatory Tailwinds

✅ Kenya: Mobile money interoperability licensed (expands addressable market)

✅ Nigeria: Central bank clarifying fintech regulation (removes uncertainty)

✅ South Africa: Spectrum auction completed (removes overhang)

✅ Regional: AfCFTA (African Continental Free Trade Area) = cross-border mobile payments

Governments are supporting digitization, not fighting it.

4. Currency Stabilization

After brutal 2024-2025 devaluations:

Nigerian naira: Stabilizing around 1,600/USD

Ghanaian cedi: Showing signs of stability

South African rand: Range-bound

As FX volatility decreases, reported earnings will reflect operational reality.

Both Vodacom and MTN have strong underlying growth masked by FX translation.

RISKS

Both Companies

FX Volatility:

40-70% of revenue in non-ZAR currencies

Rand strength = headwind, weakness = tailwind

Hedging: Limited effectiveness for operational exposure

Regulatory Risk:

Spectrum costs (Nigeria spectrum auctions)

Pricing mandates (South Africa data prices)

SIM registration requirements

Mobile money regulations

Political Risk:

Election cycles (Zambia 2026, Ghana 2024)

Policy uncertainty

Corruption/governance issues

Competition:

Airtel Africa (aggressive pricing)

MTN vs Vodacom in overlapping markets

New entrants (Starlink for satellite)

Vodacom-Specific

South Africa economic weakness (60% of revenue)

Safaricom stake illiquidity (can’t easily monetize)

International expansion execution risk

MTN-Specific

Nigeria exposure (23% of revenue, volatile)

18-country complexity (harder to manage)

IHS acquisition integration risk

Balance sheet capacity constraints

CONCLUSION

Africa’s digital infrastructure build-out is at an inflection point.

Telecom operators aren’t just beneficiaries of this transformation – they are the foundational layer enabling it.

Vodacom and MTN trade at 30-50% discounts to intrinsic value despite:

✅ Double-digit revenue growth (normalized for FX)

✅ Margin expansion from operating leverage

✅ Fintech platforms processing hundreds of billions annually

✅ Strengthening balance sheets (both cutting leverage)

✅ Upgraded management guidance

✅ Supportive macro backdrop (capital inflows, currency stabilization, regulatory clarity)

The market is pricing in:

Permanent currency headwinds (wrong – stabilizing)

Structural decline in telecom (wrong – data demand accelerating)

No value for fintech (wrong – M-Pesa/MoMo are banking platforms)

Nigeria will never recover (wrong – already recovering)

This mispricing creates opportunity.

The infrastructure is being built. The capital is flowing. The demographics are perfect.

Vodacom and MTN are how you gain exposure.

What are you seeing in African telecom? Reply in the comments or share your thoughts.